A Returns-Based Approach: Incorporating U.S. Microcap in Equity Allocations

By Ehren Stanhope

October 2017

We are often asked, “How much of a plan’s assets should be allocated to microcap equities?” As long-term investors who view the opportunity set through the lens of factors, our answer is usually some version of “Probably more than you currently do.” Microcap is a very challenging asset class to evaluate. There is little empirical research specific to the intricacies of the space, and common benchmarks cast a shadow on the alpha that is apparent in active manager returns and factor spreads. As we have written about previously,1 we believe that true microcap offers substantial opportunity for differentiated alpha generation. This paper provides an alternative framework for approaching and sizing strategic allocations to microcaps.

OPTIMIZATION MELTDOWN

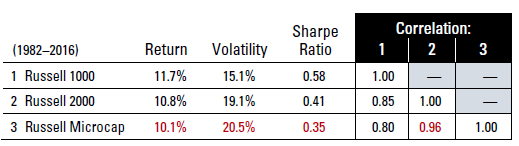

Asset allocation typically involves some form of optimization process that requires return, risk, and correlation presumptions. The table below shows common proxies for U.S. equity asset classes. As you move from top to bottom, returns decrease and volatility rises, causing decreasing risk-adjusted return (Sharpe Ratio). While lower return and higher volatility are not enough in and of themselves to eliminate an asset class from inclusion, correlations can. As one can infer from the benchmark statistics below, typical MVO (mean-variance optimization) discourages allocating to the microcap asset class.

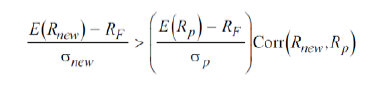

A simple test to determine the efficacy of adding an asset class to a portfolio is to look at correlation-adjusted Sharpe Ratios (see Appendix for more detail and references). To do this, simply multiply the Sharpe Ratio of an existing portfolio by its correlation with the new asset. The Sharpe of the new asset would then need to be greater than this adjusted Sharpe Ratio to be included. In the table below, both the Russell 2000® and Microcap would fail this test when compared to a 100% Russell 1000® portfolio.

While it would be easy to write off small and microcap as an asset class, a key issue we have detailed in a previous paper1 is the poor construction of the commonly used Russell Microcap benchmark. Significant overlap with the Russell 2000 Index, about 88% (as of 12/31/16), results in correlation between the indices of 0.96, resulting in little differentiation. This causes microcap as an asset class, defined by Russell, to fail simple tests for strategic inclusion in portfolios. This begs the question of whether cap-weighted benchmarks should always be the de facto measuring stick for asset classes. In researching small and microcap portfolios over the past three decades, it is abundantly clear to us that there is ample opportunity to generate return that is distinct from cap-weighted benchmarks.

A RETURNS-BASED APPROACH TO ALLOCATION

Many practitioners and academics agree that the “market” is an aggregation of stocks, weighted by market capitalization. While this is certainly accurate, we believe it represents a capacity-based view of the opportunity set.

Constructing a portfolio, or index, in proportion to market cap weights is unique in that it provides the lowest cost, highest capacity exposure to the market, regardless of investor size. It requires minimal trading beyond dividend reinvestment and investor driven flows because portfolio weights adjust in proportion to changes in market weights as stocks rise and fall. This minimizes ongoing implementation costs.

For Active managers, the proposition is that an alternative portfolio exists which will survive ongoing implementation costs required to maintain exposure to its strategy. As the size of the investable portfolio grows, aligning that portfolio more closely with market cap weights becomes a necessity, not an option because research has shown that implementation costs rise at approximately the square root of assets.2 This implicitly concentrates the bulk of investor equity exposure into more competitive portions of the market—large, liquid names. While this is great for maximizing strategy capacity, it is generally agreed that alpha becomes scarcer as market cap increases. This disadvantages larger investors relative to their smaller counterparts.

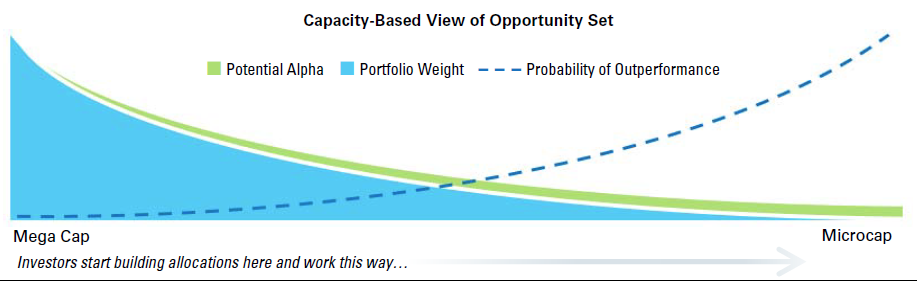

In our view, the opportunity for alpha can be defined along two dimensions: consistency and magnitude. Consistency relates to how often alpha opportunities exist; we use base rates, or batting averages to capture this concept. Strategies that win more often than they lose are predisposed to generate persistent outperformance over time. However, if the average loss is greater than the average win, the power of consistency is diminished. Investors seeking persistent and outsized gains relative to some benchmark attempt to identify situations where consistency is in their favor, and the magnitude of wins is greater than that of losses. When properly aligned, consistency and magnitude have a compounding effect over time. A capacity- based view of the opportunity set runs exactly opposite of this concept, favoring allocations where consistency and magnitude are lowest.

This chart represents a stylized capacity-based view of the equity opportunity set. Notice how the probability of outperformance is inversely related to the largest allocations:

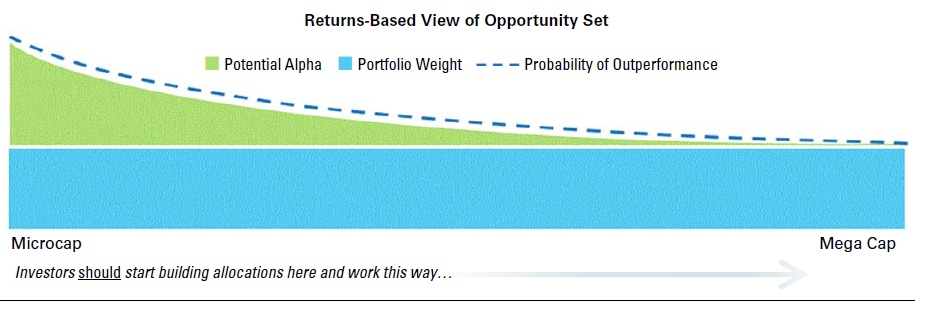

For all but the largest investors, we would argue a returns-based approach is more likely to be applicable when assessing the opportunity set. The returns-based view begins by disaggregating the effect of market cap to equalweight the opportunity set. This has the effect of pulling allocations away from the largest, most liquid names:

Viewed as a level playing field, investors would begin allocating to asset classes for which the magnitude and consistency of alpha is aligned and highest. Adjustments related to investor risk tolerances, constraints, and costs of implementation could then be made with a greater understanding of the tradeoffs associated with those decisions.

FACTOR SPREADS AS A PROXY FOR ALPHA

To evaluate the opportunity for alpha, we establish two breakpoints within the U.S. market. The first breakpoint demarcates the difference between Large Stocks, which have a market cap greater than the average across all investable stocks on the U.S. market, and Small Stocks, which have a market cap less than average. The second breakpoint sets the minimum market cap of $200 million for Small Stocks. Stocks below $200 million and greater than $50 million are designated as Microcap Stocks.3

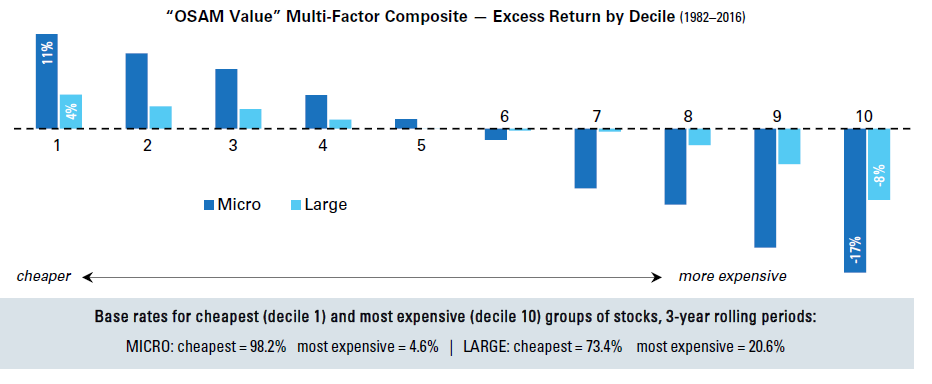

Within each asset class, we believe that factor spreads serve as a decent proxy for the availability of alpha. We define the factor spread as the return of a portfolio of stocks falling into the highest-ranked decile of a factor minus the return of a portfolio comprised of the lowest-ranked decile of a factor. In the chart below, which shows the results of investing based on our Value theme within the micro and large stock universes, respectively, this would be the difference between the excess return of decile 1 and decile 10 (28.2% for micro and 12.4% for large stocks).4 Clearly, the microcap portion of the U.S. stock market has significantly wider spreads—more than double that of Large Stocks—suggesting the opportunity to generate alpha is higher.

There are two key inferences from the chart above. First, stocks ranking in the cheapest decile within the microcap universe deliver on average nearly 3⨉ the excess return of their large counterparts. They also outperform almost 25% more often in rolling three-year periods. Second, the most expensive stocks underperform their large counterparts by 2⨉, which suggests the benefits of avoiding the most expensive stocks are much greater. This helps explain why passive allocations in small and microcap fair worse in mega and large cap. The most expensive stocks also underperform with greater consistency (95.4% of the time versus expensive large stocks which underperform only 79.4% of the time). This suggests a relatively greater opportunity for alpha generation and a wide margin for error in stock selection that provides flexibility to accommodate real world constraints.

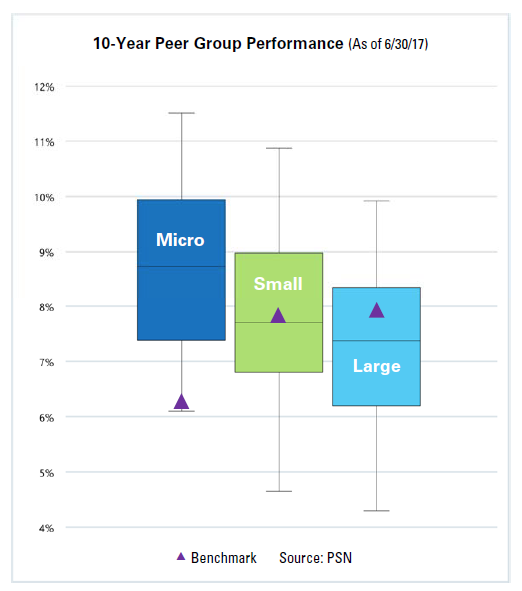

Practically, this is reflective of how the results for active management have played out over the last decade. The chart to the right shows the performance of active managers within the Micro, Small, and Large cap competitive universes. The median microcap manager outperformed the Russell Microcap benchmark by .55% (net of fees), while the median large cap manager underperformed the Russell 1000 by 0.46%. Even the 75th percentile manager in the microcap universe outperformed the Russell Microcap benchmark by 1.21%.

Notice how the performance of the median manager decreases relative to the universe, and how the spread between the top and bottom quartile manager shifts lower. This suggests to us that the magnitude and likelihood of alpha generation is inversely correlated to market cap, benchmark construction, and ultimately, the competitive nature of the space.

GENERATING RETURN “EXPECTATIONS”

One challenge we often face as quantitative investors is the idea of developing return expectations. Frankly, forecasts give a false sense of precision, and should always be taken with a grain of salt. Though we believe that over very long periods, themes like value, momentum, yield, and quality will offer investors higher riskadjusted return, we do not have the ability to forecast the next year, 3 years, or even 5 years, with any degree of certainty.

One idea that has been at the core of our philosophy is reversion to the mean. A good bit of the academic literature suggests that the factor themes mentioned above represent risk “premiums.” The concept of premiums is a bit curious to us because it is suggestive of something that is always available, whereas, factors historically come in and out of favor. A mean-reverting perspective seems a more accurate depiction of the ebb and flow that is inherent in all factors. Since factor timing is a yet unsolved mystery, we have found that a reasonable approach is consistent diversified exposure to multiple factor themes.

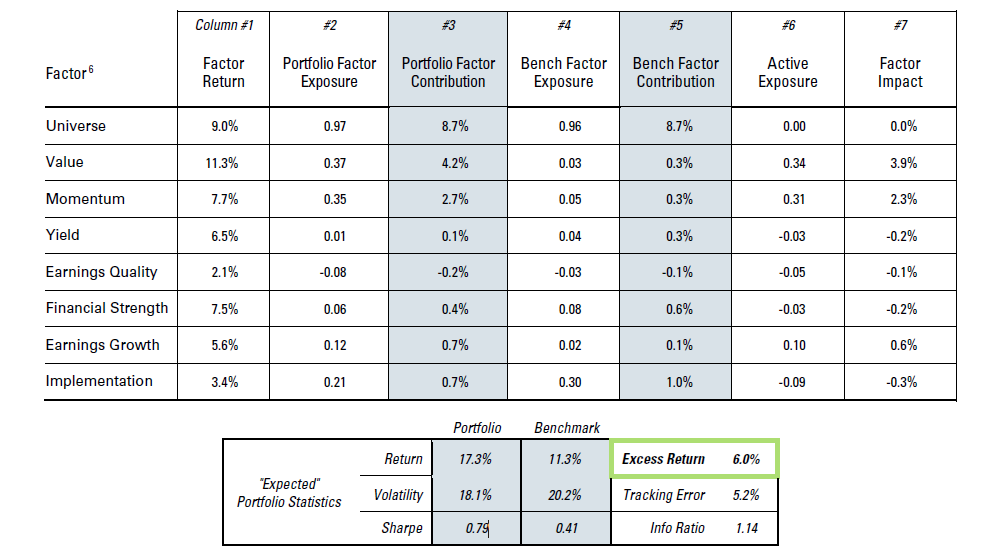

To illustrate, we created a hypothetical factor-based microcap portfolio. The portfolio is constructed by starting with our Microcap Stocks universe and eliminating stocks falling into the lowest-ranking decile by our stock selection themes of financial strength, earnings quality, and earnings growth.5 The portfolio then focuses in on stocks with the highest-ranking combined score by our Momentum and Value themes. The portfolio is refreshed monthly based on a rolling annual rebalance.

After generating a return stream for this portfolio for the 35-year period from 1982–2016, we regressed the portfolio’s return on the excess return of the highest-ranking decile of our various factor themes to generate exposures (columns 1–2 on the next page, respectively). We ran the same process for the benchmark in column 4. The contribution to return from factor exposures are in columns 3 and 5 for the portfolio and benchmark, respectively. Column 6 represents the Active Exposure—the difference in exposure for the portfolio and benchmark. Finally, column 7 decomposes the Factor Impact on the portfolio’s excess return. Using the Value line item as an example, the cheapest (highest-ranked decile of stocks) by our Value theme outperformed the universe return of 9.0% by an annualized 11.3% excess return. The portfolio had a 0.34 overweight exposure to Value, which contributed annualized excess of 3.9% to return over the full period.

Based on the results of this 3½-decade study, we make the intellectual leap that factor excess returns, volatility, and correlation in the future will somewhat resemble those of the past. Over reasonable time frames, this has been a decent assumption.6

Volatility, risk-adjusted return (Sharpe), and “expected” return can be found at the bottom of the table. Since absolute returns are incredibly difficult—if at all possible—to predict, the more instructive info is likely the excess return, tracking error, and information ratio. The table is suggestive that this factor-based portfolio, which demonstrates strong active exposures to value and momentum, should generate excess return of 6.0% over the long term. For perspective, this level of excess return would be representative of the 5th percentile manager within the microcap manager peer universe over the past 10 years. A key assumption that cannot be emphasized enough is consistent factor exposure throughout the period. For example, if this hypothetical strategy started buying growth stocks without regard to valuation in the 1990s, this data becomes irrelevant. Discipline to any strategy is key to avoid any behavioral pitfalls in the future.

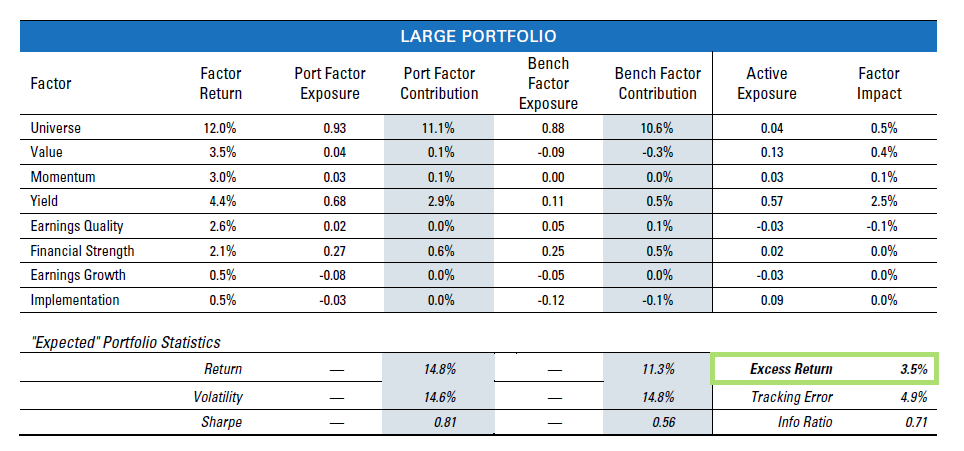

We performed similar exercises to generate factor-based portfolios within our Large and Small stock universes. To provide some diversification of factor exposure across the universe, the Large Portfolio uses Shareholder Yield as its final selection factor, and the Small Portfolio uses our Value theme.

In both cases, factor exposures are about as expected, the Small Portfolio had strong active value exposure with benchmark-like quality and momentum exposure. The Large Portfolio had strong active Shareholder Yield exposure, and mostly benchmark or better elsewhere. In both cases, the “expected” excess is on par with top active managers over the previous 10 years, as illustrated above.

DETERMINING ALLOCATIONS

Finally, having generated expectations for excess return and volatility in Micro, Small, and Large portfolios, we can apply the results in the common MVO (mean-variance optimization) framework to determine overall equity portfolio weights.

The inputs required for MVO are expected returns and covariances. We use the expected returns generated in the analysis above as inputs. The return streams for the portfolios are then used to generate a covariance matrix. Implicit is the assumption that covariances are stationary over time. We know this not to be the case in the short term, so care should be taken to interpret the results only in the context of long-term strategic, not tactical, decisions. The correlation matrices below demonstrate the differentiated return profile that can be generated with carefully constructed factor portfolios as distinct from relying on market cap-weighted benchmarks in asset allocation. Notice the decrease in correlation between the Micro and Small portfolios and the Russell 2000 and Russell Microcap benchmarks.

Equipped with expected returns and covariances, we apply very few constraints to the overall portfolio optimization. We require the portfolio to be fully invested at all times; shorting is not allowed. Other than that, no constraints are needed to “force” the optimization into reasonable results. The objective is maximizing riskadjusted return, as measured by the Sharpe Ratio.

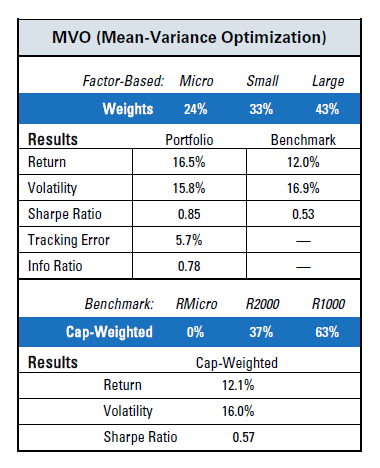

The first table below displays the results of the MVO process. Weighting to the Micro and Small portfolios are much greater than most allocators are probably used to (a combined 57% of the equity portfolio). The lower portion of the table includes summary statistics for our hypothetical optimization of the micro, small, and large factor portfolios as compared to the cap-weighted benchmarks at the optimization weights. Contrary to what might be commonly expected, the increased allocations do not result in dramatic increases in volatility. Volatility actually decreases by 1%. With 4.5% annualized excess return and 1% lower volatility, the Sharpe Ratio increases dramatically.

As a comparator, we ran a parallel comparison (lower table) that uses expected returns and volatility for the Russell benchmarks as proxies for cap-weighted portfolios. The results are aligned much more closely with typical investor allocations, though still probably higher on small cap than expected.

Thus far, we have not considered the risk tolerance of the allocator. While one set of investors may be perfectly comfortable with significant micro and small cap exposure, it is understandable that certain investors may need to adjust portfolios to their risk preferences.

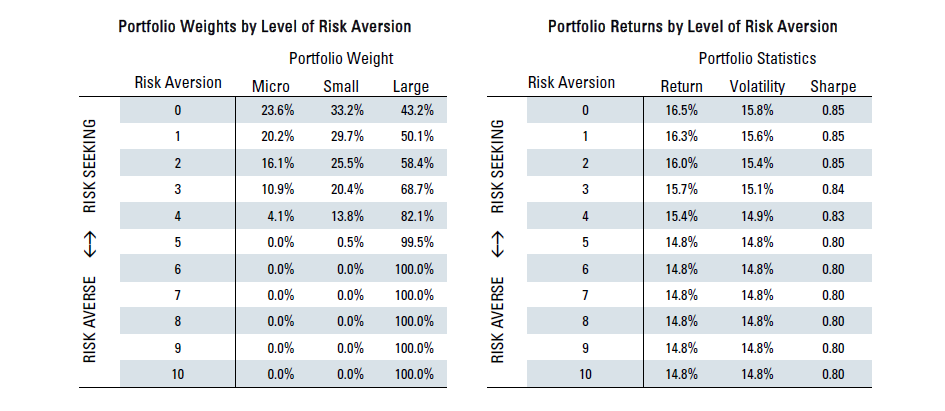

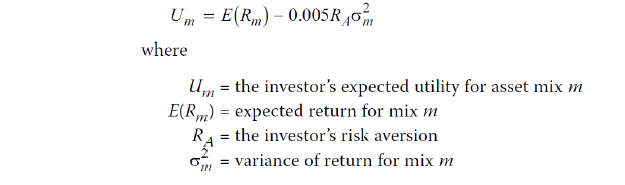

It turns out that there is a relatively simple way to scale portfolio returns based on volatility. This entails incorporating a penalty factor for portfolios that adjusts based on an investor’s risk aversion. Risk averse investors would incorporate a greater penalty in determining their appropriate policy portfolio. Less risk averse investors would incorporate lower penalties. Risk aversion could be modeled to incorporate any number of different characteristics—investment horizon, sensitivity to absolute and/or relative drawdowns, liquidity needs, etc. For our purposes, we demonstrate an example based on volatility

In the table below, a Risk Aversion score of zero represents the utility of each portfolio for a risk seeking investor, effectively the results we determined in the MVO analysis above. We then apply successively increasing risk penalties based on the volatility of each portfolio. Because the Micro and Small portfolios are more volatile than Large cap, returns decrease to the point at which the utility of the Micro and Small portfolio are close to indifferent with Large by the time a risk aversion score of 5 is reached. Think of the returns below as a proxy for how the investor feels about the level of return given the volatility required to achieve that return. A highly risk-averse investor with a score of 10 significantly prefers the Large cap portfolio rather than Small or Micro.

These utility-adjusted returns can then be used as expected return inputs into additional MVO analysis which adjusts allocations of the total equity portfolio for individual risk aversion. The table below displays these results at each level of risk aversion. As risk aversion increases, the optimal weight dials down exposure to the Micro and Small strategies in favor of the lower volatility large strategy.

CONCLUSION

It would behoove of allocators to recognize traditional indexes for what they are, factor-based strategies predicated on one factor, market cap. Though market cap has everything to do with low cost implementation, high capacity, and cheap beta exposure, it has little to do with optimal investor allocations for all but the largest plans.

Breaking from the capacity-based, cap-weighted perspective allows allocators to focus on asset classes in which "edges" are apparent and hidden within traditional benchmarks. Allocators should view portfolios through the lens of consistent factor exposures over multiple market cycles. Doing so allows for reasonable "expected" excess returns that are otherwise overshadowed by cap-weighted indexes when used as proxies for asset class returns. Further, poor benchmark construction can, in and of itself, actually eliminate entire asset classes from consideration.

Using data from the longest timeframe available to OSAM Research, we input the factor excess, correlation, and risk aversion into traditional MVO analysis. The results are surprising, suggesting that volatility is reduced and returns are improved after micro and small cap stocks including in equity asset allocation.

APPENDIX

Decision to Add the Asset Class

For an investor deciding to gain exposure to an asset class, the decision itself can be addressed through common frameworks that seek to balance risk-return tradeoffs. Blume (1984) and Elton, Gruber, and Rentzler (1987) suggest that the decision to add an asset class to an existing portfolio can be determined by comparing the Sharpe ratio of the new asset class with the correlation adjusted Sharpe ratio of the existing portfolio. The correlation adjustment is important as it incorporates the benefits of risk reduction when evaluating the new asset.

Factor Theme Descriptions

Universe — We define the market factor as our equal-weighted selection universe for the portfolio.

Value — We measure Value as the excess return of the highest-ranking decile of our Value Composite relative to our selection universe. Our Value Composite consists of underlying constituents such as price relative to sales, earnings and cash flows.

Momentum — We measure Momentum as the excess return of the highest-ranking decile of our Momentum Composite relative to our selection universe. Our Momentum Composite consists of four underlying constituents—3-month, 6-month, and 9-month momentum, and 12-month volatility.

Yield — We measure Yield as the excess return of the highest-ranking decile of Shareholder Yield relative to our selection universe.

Earnings Quality — We measure Quality as the excess return of the highest-ranking decile of our Earnings Quality Composite relative to our selection universe. The composite consists of several underlying constituents, which measure the conservatism of accounting choices through accruals.

Financial Strength — We measure this factor as the excess return of the highest-ranking decile of our Financial Strength Composite relative to our selection universe. The composite consists of multiple underlying constituents, which assess balance sheet leverage and strength.

Earnings Growth — We measure this factor as the excess return of the highest-ranking decile of our Earnings Growth Composite relative to our selection universe. The composite consists of multiple underlying constituents, which measure the consistency of earnings and profitability.

Implementation — We measure the cost of implementation using two factors that historically correlate with the cost of trading, such as dollar volume and market cap.

Factor Correlations

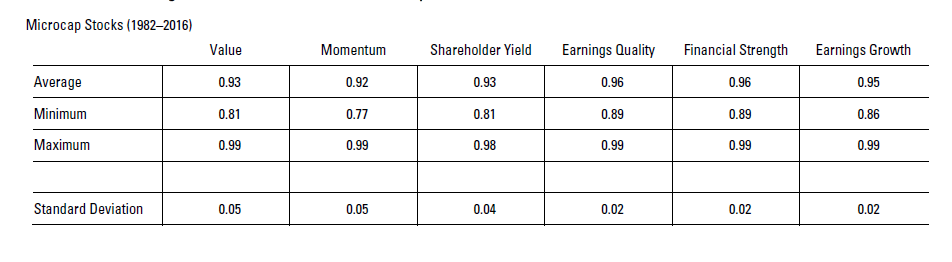

The table below includes summary stats for the rolling 36-month correlation of the highest-ranked decile of six factor themes encompassing value, momentum, yield, and quality relative to the microcap universe. Correlations are on average above 0.9, with deviations within reasonable bounds.

Statistics from Rolling 36-month Correlation with Microcap Universe

Risk Aversion

Risk aversion can be proxied through utility theory. Practically, the return of a portfolio can be adjusted through a penalty factor for increased volatility. Risk averse investors would incorporate a greater penalty in determining their appropriate policy portfolio. Less risk averse investors would incorporate lower penalties based on increases in risk. Risk aversion could be modeled to incorporate a number of different characteristics— investment horizon, sensitivity to absolute and/or relative drawdowns, liquidity needs, etc. In Zvi Bodie’s 2004 Investments, the authors outline a simple equation for modeling risk aversion.

GENERAL LEGAL DISCLOSURES & HYPOTHETICAL AND/OR BACKTESTED RESULTS DISCLAIMER

The material contained herein is intended as a general market commentary. Opinions expressed herein are solely those of O’Shaughnessy Asset Management, LLC and may differ from those of your broker or investment firm.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by O’Shaughnessy Asset Management, LLC), or any non-investment related content, made reference to directly or indirectly in this piece will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this piece serves as the receipt of, or as a substitute for, personalized investment advice from O’Shaughnessy Asset Management, LLC. Any individual account performance information reflects the reinvestment of dividends (to the extent applicable), and is net of applicable transaction fees, O’Shaughnessy Asset Management, LLC’s investment management fee (if debited directly from the account), and any other related account expenses. Account information has been compiled solely by O’Shaughnessy Asset Management, LLC, has not been independently verified, and does not reflect the impact of taxes on non-qualified accounts. In preparing this report, O’Shaughnessy Asset Management, LLC has relied upon information provided by the account custodian. Please defer to formal tax documents received from the account custodian for cost basis and tax reporting purposes. Please remember to contact O’Shaughnessy Asset Management, LLC, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you want to impose, add, or modify any reasonable restrictions to our investment advisory services. Please Note: Unless you advise, in writing, to the contrary, we will assume that there are no restrictions on our services, other than to manage the account in accordance with your designated investment objective. Please Also Note: Please compare this statement with account statements received from the account custodian. The account custodian does not verify the accuracy of the advisory fee calculation. Please advise us if you have not been receiving monthly statements from the account custodian. Historical performance results for investment indices and/or categories have been provided for general comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your account holdings correspond directly to any comparative indices. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. O’Shaughnessy Asset Management, LLC is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. A copy of the O’Shaughnessy Asset Management, LLC’s current written disclosure statement discussing our advisory services and fees is available upon request.

The risk-free rate used in the calculation of Sortino, Sharpe, and Treynor ratios is 5%, consistently applied across time.

The universe of All Stocks consists of all securities in the Chicago Research in Security Prices (CRSP) dataset or S&P Compustat Database (or other, as noted) with inflation-adjusted market capitalization greater than $200 million as of most recent year-end. The universe of Large Stocks consists of all securities in the Chicago Research in Security Prices (CRSP) dataset or S&P Compustat Database (or other, as noted) with inflation- adjusted market capitalization greater than the universe average as of most recent year-end. The stocks are equally weighted and generally rebalanced annually.

Hypothetical performance results shown on the preceding pages are backtested and do not represent the performance of any account managed by OSAM, but were achieved by means of the retroactive application of each of the previously referenced models, certain aspects of which may have been designed with the benefit of hindsight.

The hypothetical backtested performance does not represent the results of actual trading using client assets nor decision-making during the period and does not and is not intended to indicate the past performance or future performance of any account or investment strategy managed by OSAM. If actual accounts had been managed throughout the period, ongoing research might have resulted in changes to the strategy which might have altered returns. The performance of any account or investment strategy managed by OSAM will differ from the hypothetical backtested performance results for each factor shown herein for a number of reasons, including without limitation the following:

- Although OSAM may consider from time to time one or more of the factors noted herein in managing any account, it may not consider all or any of such factors. OSAM may (and will) from time to time consider factors in addition to those noted herein in managing any account.

- OSAM may rebalance an account more frequently or less frequently than annually and at times other than presented herein.

- OSAM may from time to time manage an account by using non-quantitative, subjective investment management methodologies in conjunction with the application of factors.

- The hypothetical backtested performance results assume full investment, whereas an account managed by OSAM may have a positive cash position upon rebalance. Had the hypothetical backtested performance results included a positive cash position, the results would have been different and generally would have been lower.

- The hypothetical backtested performance results for each factor do not reflect any transaction costs of buying and selling securities, investment management fees (including without limitation management fees and performance fees), custody and other costs, or taxes – all of which would be incurred by an investor in any account managed by OSAM. If such costs and fees were reflected, the hypothetical backtested performance results would be lower.

- The hypothetical performance does not reflect the reinvestment of dividends and distributions therefrom, interest, capital gains and withholding taxes.

- Accounts managed by OSAM are subject to additions and redemptions of assets under management, which may positively or negatively affect performance depending generally upon the timing of such events in relation to the market’s direction.

- Simulated returns may be dependent on the market and economic conditions that existed during the period. Future market or economic conditions can adversely affect the returns.