O'Shaughnessy Quarterly Letter Q4 2019

By Patrick O’Shaughnessy

January 2020

O’Shaughnessy Quarterly Investor Letter Q4 2019

January 8, 2020

Dear Investor,

In 2019, we completed more research than in any prior year, built and launched CanvasTM, and shared 13 papers and over 50 podcasts. We grew our team and operated with more focus than in any year I can remember. As of the end of the year, we are managing $5.7B in assets under management, across 2,508 accounts for individual and institutional investors.

I joked at our holiday party that I felt like I aged 5 years in 2019—but I wear the age with pride. I’ve never learned so much in a single year, and I’m confident everyone on the team could say the same. More than anything, I will remember 2019 for how hard and efficiently the OSAM team worked. They redefined what I thought was possible in a single year.

In this letter I’ll discuss where we stand in markets at year end, and discuss what we built and learned at OSAM during the year.

Market Observations and Outlook

In 2019, growth beat value yet again. But the reasons this year were different. Most of growth’s strong run vs. value this past decade has been the result of better business results. Growth stocks simply trounced value stocks when it came to fundamental earnings growth. But in 2019, the story was flipped. This year growth’s dominance was fueled entirely by multiple expansion and not by good business results or return of capital to shareholders (where value fared much better).

As a result, at the end of 2019, growth stocks were trading at expensive multiples with high and rising expectations. Value stocks traded at moderate multiples with low and falling expectations.

Thanks in large part to the multiple expansion in growth stocks, the overall market has grown more expensive and is priced for weaker returns over the next decade than we saw over the previous decade. We believe in value as a structural strategy (it is one of 6 primary factor categories and one of 3 primary selection factors that we use) but are especially excited at its prospects given where value stocks are positioned relative to growth and the rest of the market.

***

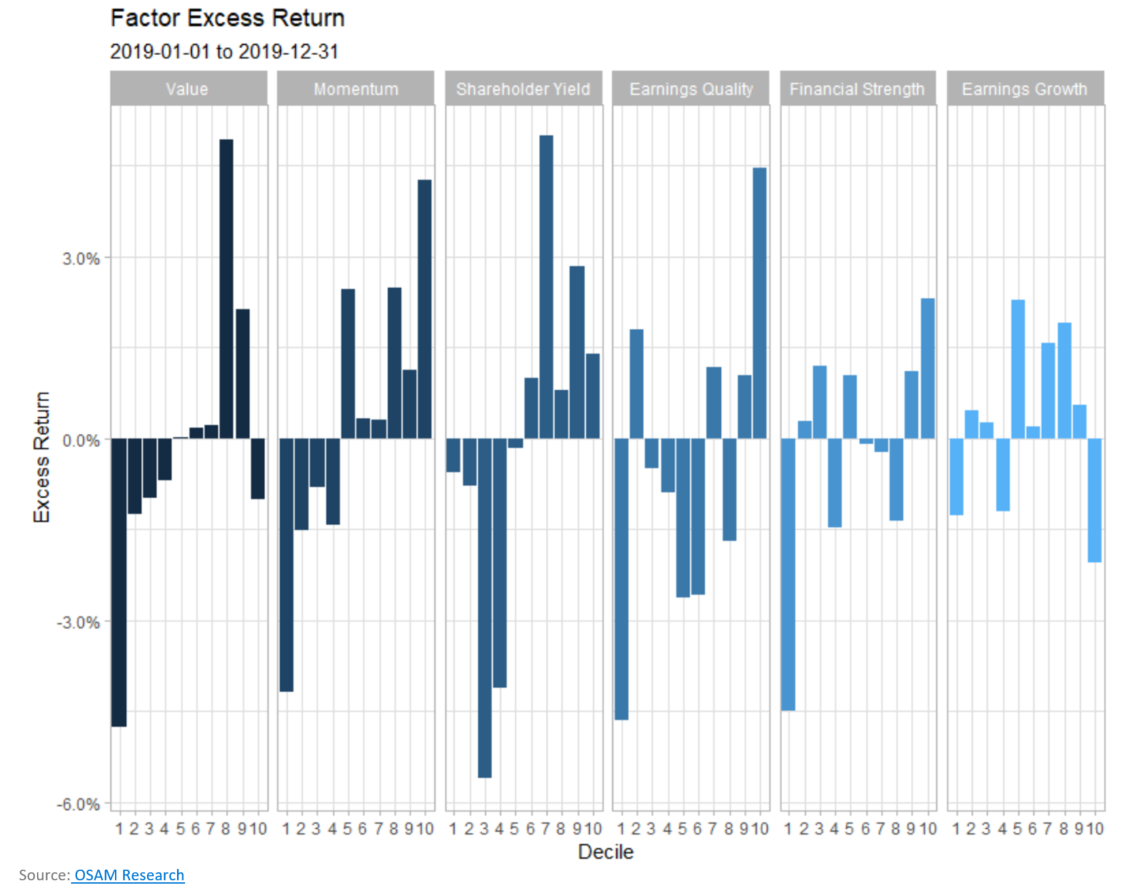

Traditional factor investing had a rough year. While we outperformed slightly in our largest strategy (“Market Leaders Value”) relative to the benchmark, the rest of our strategies struggled. This grid shows the decile performance of our six primary factor themes. As a factor investor, you’d prefer that the first decile of each factor outperform. But during 2019, every single “highest decile” factor portfolio performed poorly.

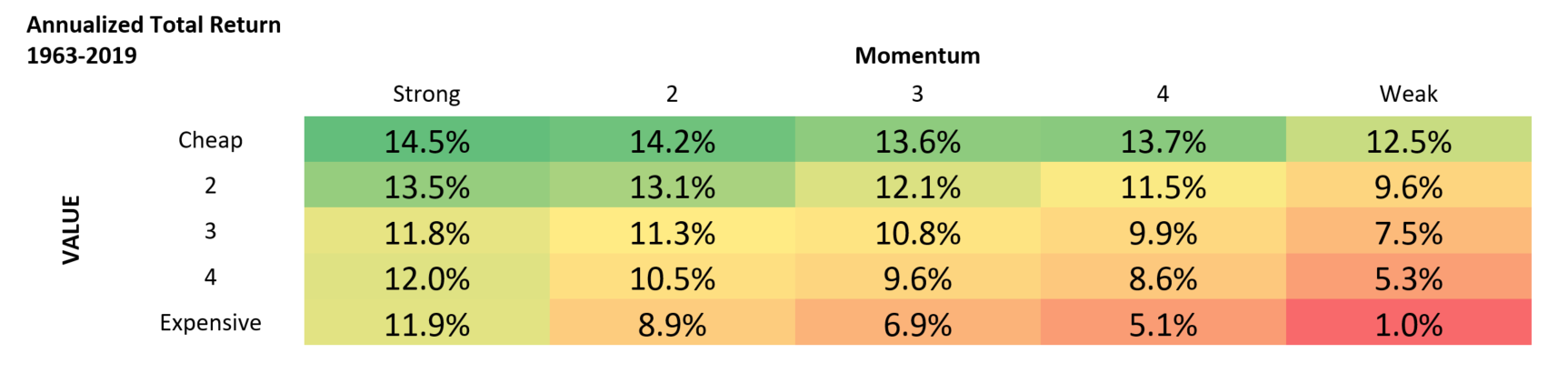

Digging a bit deeper to see how factors interacted, we see more evidence of it being a hard year for quants. Across available history, a better place to invest was in stocks with cheap valuations and strong momentum. But in 2019, the category of “cheap momentum” delivered a +16.1% return—the lowest of any valuation/momentum segment. Expensive momentum stocks did much better and delivered a +35.3% return in 2019.

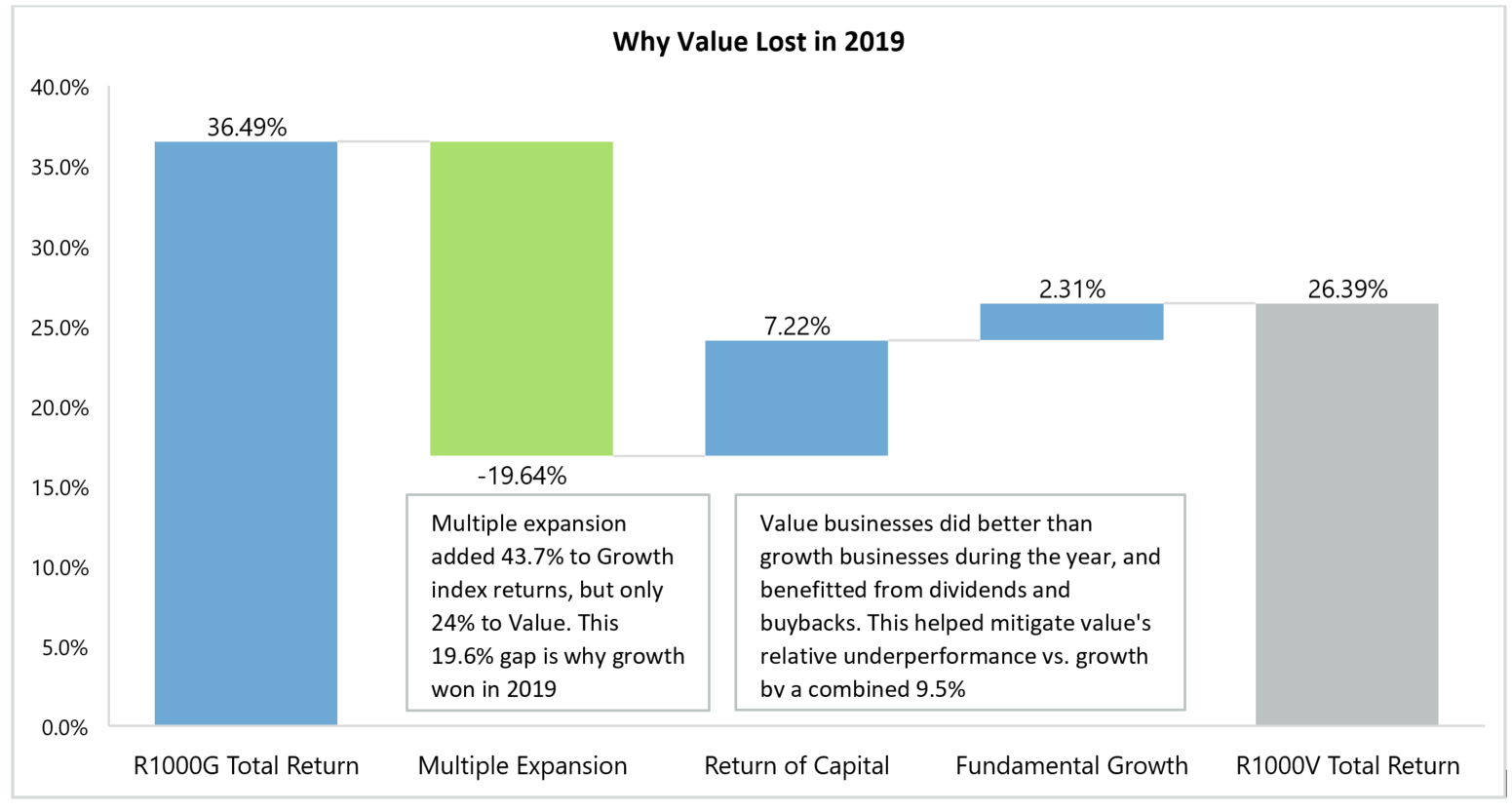

The table below segregates Russell style index performance for 2019 into three simple return buckets: return from dividends and buybacks (“return of capital”), return from fundamental growth, and return from multiple expansion.

Value stocks delivered better fundamental performance (-1.22% contribution for value vs. -3.53% for growth) and delivered positive returns via dividends and buybacks (adding +3.58%), while the growth index diluted shareholders (detracting -3.64%). This means that had changing valuation multiples not affected returns and we instead only cared about business growth and return of capital; the Russell 1000 Value would have outperformed the Russell 1000 Growth by 9.5% in 2019.

But multiple expansion matters, and for the Russell 1000 Growth, multiple expansion contributed a whopping 43.7% to returns. Value multiples expanded too, but the effect was half as strong, boosting returns by 24.0%. Add it all up, and despite much weaker business performance, growth still beat value by 10.1%.

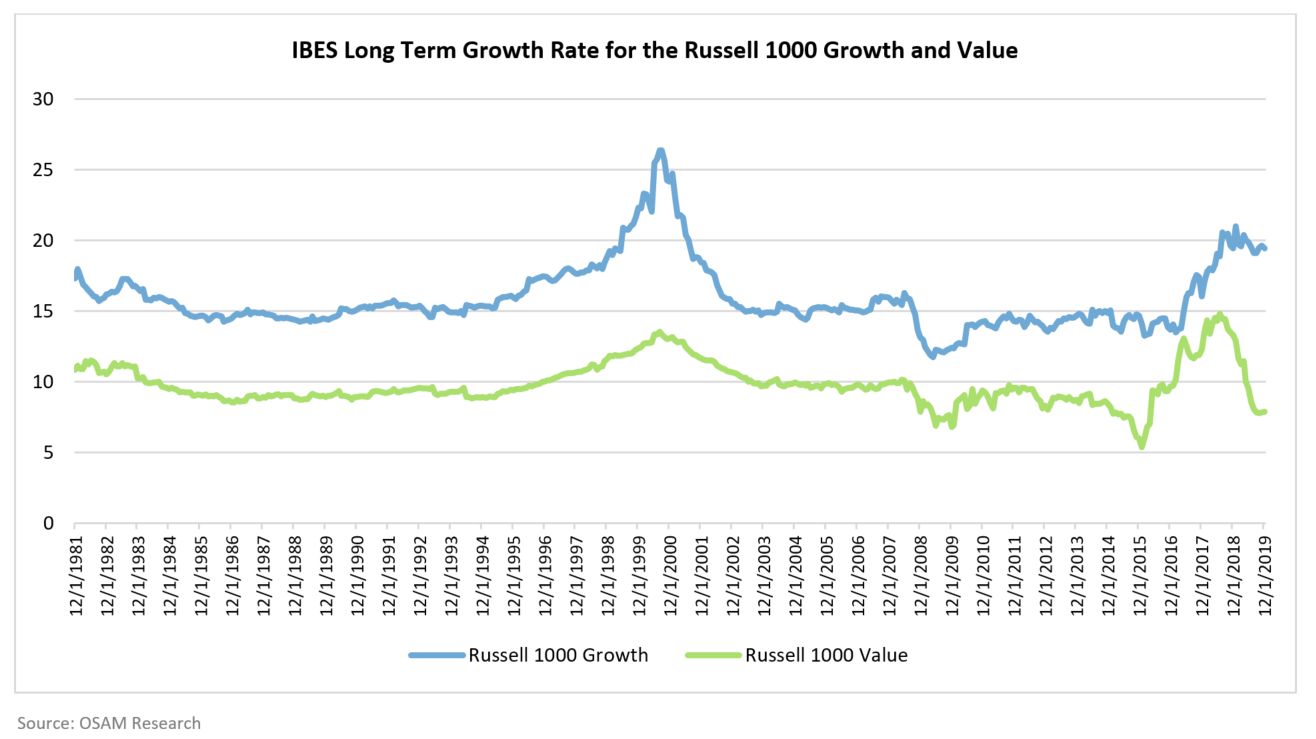

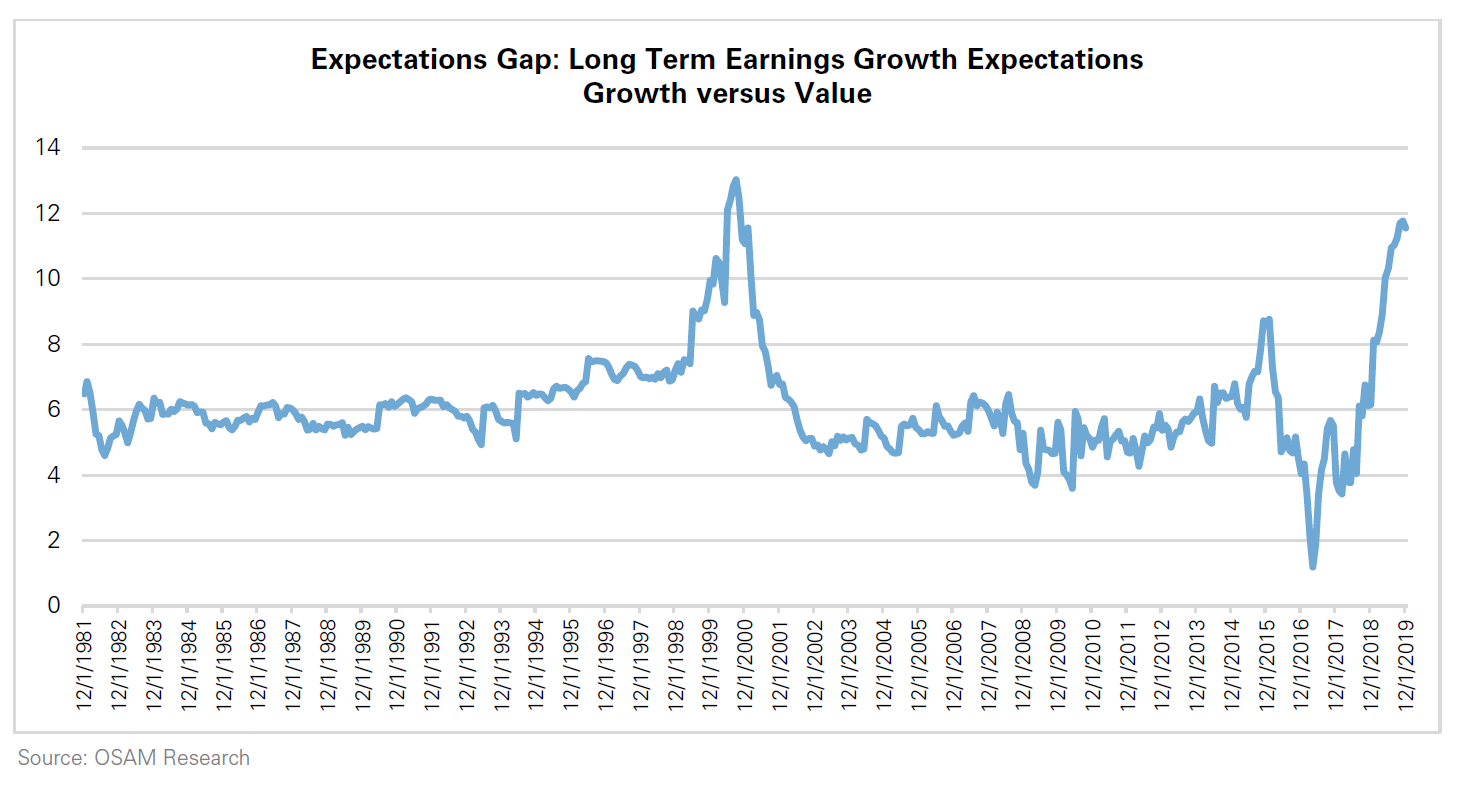

When we look closely at the widening valuation spread between cheap and expensive segments of the market, we see that that it’s based on increased optimism around the future prospects of growth stocks and increased pessimism around the future prospects of value stocks. To illustrate this disparity, the charts below show the average estimates for long-term earnings growth collected by IBES. Analysts are expecting growth companies (those in the Russell 1000 Growth index) to grow their earnings at ~20% per year over the long-term, and for value companies to grow their earnings at only ~7% per year.

As you can see, the spread between the estimates has recently blown out, and now sits within striking distance of the March 2000 extreme:

Growth dominated the 2010s because of great real business performance, but now, after a bad year for the growth companies themselves, analysts have the second highest set of future earnings expectations for growth stocks (both in absolute terms and relative to value) since 2000.

What About the Broad Market?

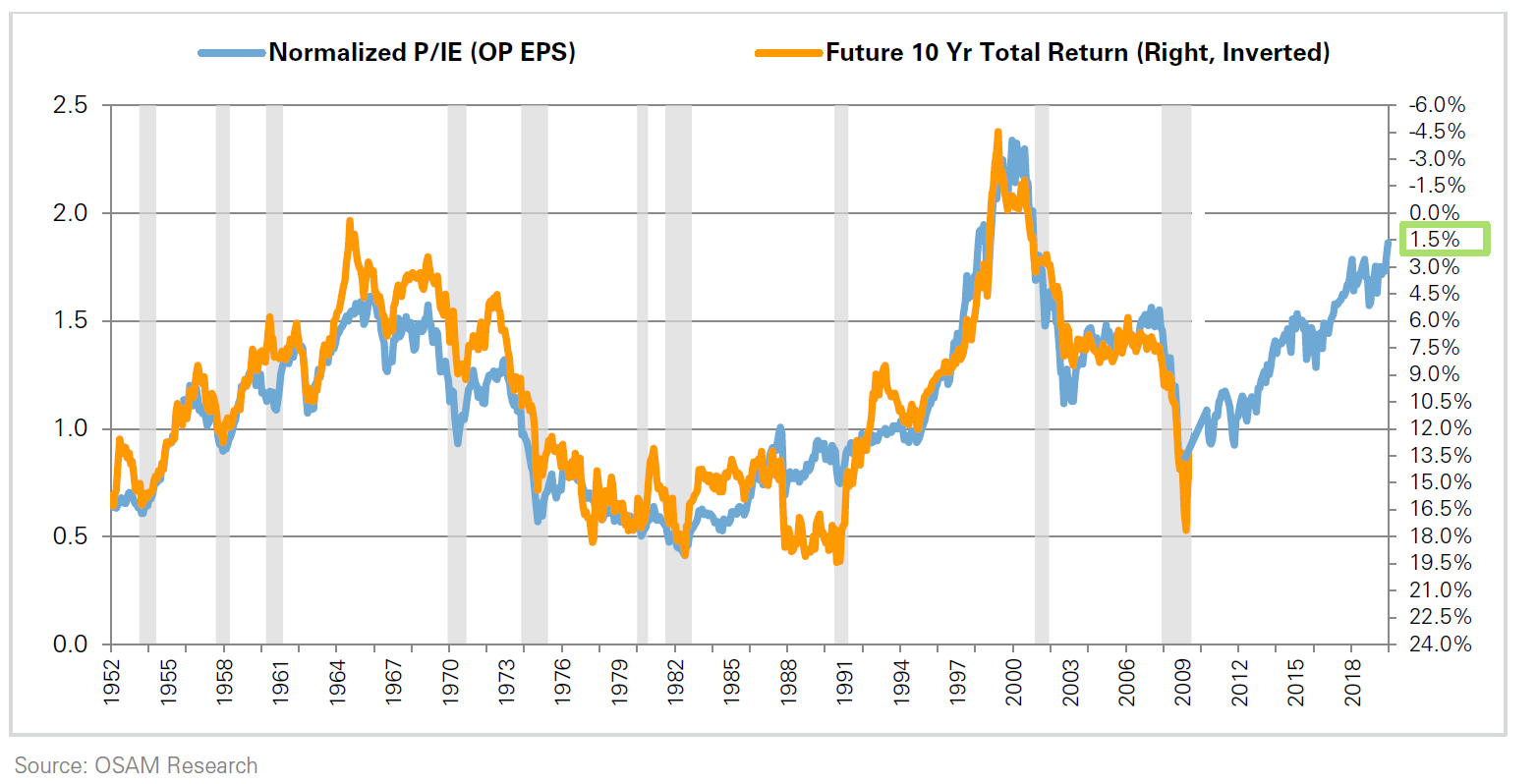

As the chart below illustrates, our updated in-house 10-year point estimate for the U.S. market’s nominal total return fell during the year, and now sits at ~1.5% annualized, which would mean a ~16% total return over the next decade.1 If this estimate turns out to be accurate (it might not), the next decade will end up being one of the weakest periods for equity returns on record.2 We are generally skeptical of forecasts in markets, and offer this only as a strategic guide or starting point for forming return expectations—it does not affect our investing strategies in any way (which we expect to perform considerably better than the overall market).

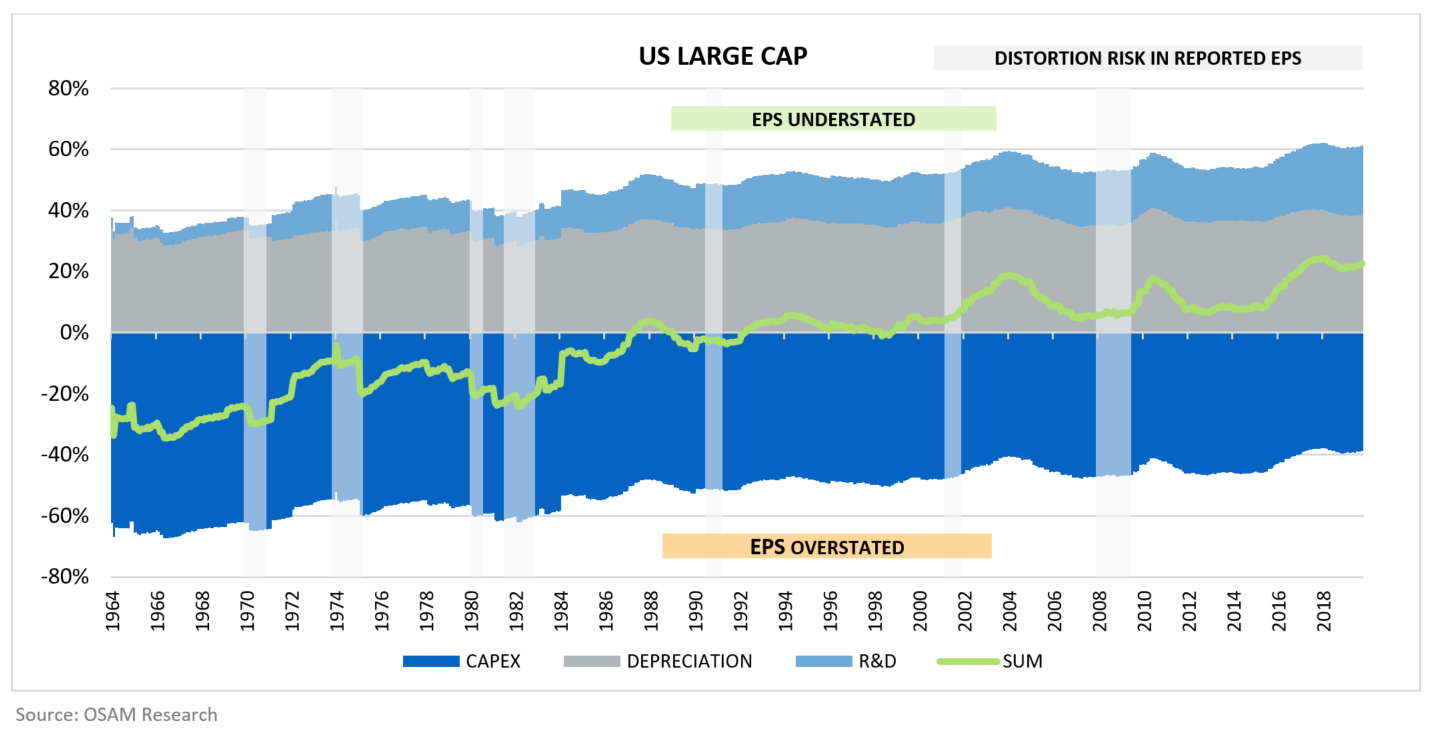

On a more positive note, there is some evidence that the corporate earnings that feed into market valuation measures, ours included, are understated relative to history. If true, this observation would mean that we should expect future returns to be somewhat higher than the returns that markets at similar valuations in the past ended up producing.

Why are earnings today understated relative to history? In part because companies today spend less on capital expenditures (a deferred expense that gets smoothed out over a number of years) and more on research and development (a current expense that hits earnings immediately, with no deferral). So, today’s earnings tend to be “sandbagged” relative to the past.3

The message is still the same: long-term returns for the overall U.S. equity market are likely to be weak going forward. This point has been made for some time now, and it reflects a reality that many of us have already come to terms with. Unfortunately, it doesn’t answer the real question, which is the question of what to do with a portfolio, right now. Equities may be priced for low returns, but other asset classes, most notably fixed-income and cash, are priced for even lower returns.

What, then, should investors do? We think that the answer is to do what successful investors did in the early 2000s, which was to focus on the opportunities presented inside the market. We believe that value stocks are providing an opportunity today that is similar (though not identical) to the opportunity that they presented then.

I’m fully invested in equities. But the price (multiple) that I pay for my portfolio today, measured relative to earnings, sales, and free cash flow is significantly lower than the price of the Russell 1000. My OSAM Canvas portfolio, which represents nearly all my public equity exposure, trades at 15x earnings and 9x cash flow. The Russell 1000 trades at 23x earnings and 14.7x cash flow. My total portfolio shareholder yield is 5.1%. The Russell 1000’s is only 2.6%. I share these points because these kinds of value-based considerations have historically been useful predictors of future returns. There’s a very real opportunity right now to improve upon the returns of the broad market using systematic strategies that incorporate them.

The bottom line: we believe in equities and systematic strategies for the long haul and believe that value is set up for strong returns relative to growth but believe that expectations for equity market return over the next decade should be tempered.

Canvas

Our goal with Canvas is to supercharge the advisers who use it by making fully customized portfolios possible for the first time. Funds (mutual funds and ETFs) dominated the last 100 years of investing. Fully customized portfolios—unique strategies built to suit each investor, managed inside individual separate accounts—will dominate the next 100. Fully customized portfolios are possible through the combination of research and technology, which is where we excel. Canvas created this category, and we will continue to lead it.

We began building Canvas at the beginning of this year, launched it publicly in September at the Wealth/Stack conference, and began trading customized Canvas portfolios for clients in early November.

Following the prescient advice of Chetan Puttagunta (a General Partner at Benchmark Capital and soon-to-be a podcast guest), we decided that we’d launch the product by finding a small group of early partners—what we call our “First 10”—and then close the door to new firms, which we have since done.

These firms are all independent registered investment advisers, which manage an average of $2.2 billion. They are all over the country, with different firm structures and client types, so that we can learn from each.

Two interesting observations since our first client account opened on November 5th:

First, of the First 10 firms, no two firms have the same basic strategy settings (asset allocation, or balance between passive and factor exposure). This means each RIA is using Canvas to build their firm’s investment philosophy into systematic strategies in unique ways.

Second, across the new individual Canvas portfolios we’ve opened so far, the majority have entirely unique strategy settings, tailored to the individual investor. So even within specific RIA firms, Canvas is being used to build different strategies for different individual clients. Already there are two levels of customization—firm level and client level—which is exactly what we designed Canvas to do.

Canvas is a new product but also a new mindset for us at OSAM. Seeing customization happening real time has shifted our orientation from fixed to flexible strategy and product design. We’ve realized that the idea of tailoring systematic strategies to the end investor is a powerful concept, and we believe it is the future of systematic asset management for both individuals and institutions.

Once we feel we’ve refined and expanded Canvas’s capabilities based on time spent with the First 10, we will open the gates and do the same thing again: find another cohort of partners, hopefully with more unique problems to be solved, and iterate the platform.

Lessons from Building Software

I think everyone would benefit from building client facing software. Doing so helps you understand your clients in the deepest way possible. In the past, when we’ve asked clients what problems they are trying to solve, we didn’t get actionable answers. In sharp contrast, when we demo a flexible software chassis like Canvas to prospects, they project their real problems onto the software in the form of the question: “Can it also do x?”

We track the list of these questions carefully, and they have heavily influenced our product roadmap. Critically, we aren’t just asking customers what they want and building it—not at all. Instead we are combining our distinct understanding of systematic investing strategies and software and laying it alongside our First 10’s deep understanding of their clients to arrive at the most valuable new additions or refinements to the Canvas platform.

We’ve also learned that ease and efficiency of use is critical—a mindset which bleeds into other non-software work. Here’s Chetan describing how a business user thinks about whether to adopt a new software system:

"This [new software] is yet another system that your prospective client has to interact with. Ultimately, what you deliver from your software is not actually your customer’s job. Your customer has an end goal. If they’re in sales, they’re trying to sell more. If they’re in marketing, they’re trying to market more. If they’re in financial services, perhaps they’re trying to lend more. If they’re in manufacturing, they’re trying to manufacture more. There is some end goal that your customer is trying to achieve and becoming proficient in your software system is *not*the end goal of your customer, so aligning proficiency of your software solution to your customer’s end goal is critical."

This makes me think of one of my favorite books, by Steven Pressfield called Nobody Wants to Read Your Sh*t. As Pressfield writes,

"Nobody wants to read your sh*t. What’s the answer? 1) Streamline your message. Focus it and pare it down to its simplest, clearest, easiest-to-understand form. When you understand that nobody wants to read your sh*t, your mind becomes powerfully concentrated. You begin to understand that writing/reading is, above all, a transaction. The reader donates his time and attention, which are supremely valuable commodities. In return, you the writer must give him something worthy of his gift to you."

It’s helpful to remember no one wants to adopt your thing...unless it’s extremely useful to help them achieve their end goal. Take the above paragraph and substitute your area of work (software building or otherwise) for “writing/reading,” and you have a powerful business lesson—one we are trying to follow at OSAM.

Research + Factors

We’ve been refining our core factors—value, momentum, business quality, and shareholder yield—for nearly three decades. We expect to continue to improve on these core factors, and we did so in 2019.

Following the deep exploration of corporate profitability by OSAM Research Partner “Jesse Livermore+”, we completed a research project which led to an improvement in how we measure a company’s growth profile. We updated our production models with this new signal, which represented an improvement over our old method of measuring profitability and growth.

Without going into the somewhat painstaking detail on the factor research, the headline is free cash flow works brilliantly alongside side earnings as the “profit” measure inside of factors like return on capital, per share growth, and profitability breakouts (above or below a company’s historical trendline).

This year, we also made massive learning leaps as a team in categories outside of the core factors. Specifically, in the areas of corporate innovation, machine learning, portfolio optimization, risk modeling, after tax returns & tax alpha, and ESG.

We are excited about ongoing projects working deeper into risk modeling, transaction cost modeling, portfolio optimization, and “greenfield” factor research like innovation modeling. Each area of research represents a way for us to build more efficient and unique factor strategies for clients.

Acts of Kindness

At the end of every podcast, I ask the guest for the kindest thing that anyone has ever done for them. The answers make me emotional every time, and serve as great reminders for how to live.

In the spirit of that question, here are the acts of kindness in business for which I’m thankful this year.

I am most thankful for the OSAM team and their families, our research partners, and our investing clients. I don’t have space in this letter to detail the number of new skills the team picked up this year. My favorite part of the environment we’ve built is the curiosity and collaboration evident in every interaction. This year has been a business adventure beyond all maps.

I am thankful to Brent Beshore, Bill Hessert, and Jeremiah Lowin for their constant advice and support. Brent is a business partner twice over (via his firm’s permanent equity fund and an investor retreat that he and I co-host called Capital Camp, but he is also a dear friend who has forgotten more about business than I’ll ever know. Bill is a friend who I call for just about everything. He is insanely smart and adventurous. I joke that I’ve been waiting since 1st grade to invest in a company run by Jeremiah, and we finally got the privilege to do so. Watching him build a company has blown me away and saved me so much time because he’s generous in sharing what he is learning at the frontier of technology.

I am thankful for the lessons Graham Duncan, Sam Hinkie, and Jim O’Shaughnessy have taught me about people and trust. Sam maintains a folder he calls “stunning colleagues.” Graham says, “talent is the best asset class.” My father delivers on what he commits to every single time. Each has taught and shown me how to invest in people and in relationships.

I am thankful for the example set by Bill Gurley, Josh Wolfe, Michael Mauboussin, Bethany McLean, Zack Kanter, Daniel Ek, and Sarah Tavel. Their thinking—often shared in writing—reveals bottomless curiosity about business and investing. I’ve already mentioned Chetan Puttagunta, but I need to say again how thankful I am for his advice and enthusiasm. He has been a personal Yoda for me as we’ve tackled the world of software.

Nothing excites me more than the prospect of decades of compounding ahead, working with these people and more like them to build what we believe will be the best investing platform on the planet.

Continuing the OSAM Way

One of my favorite questions to ask other investors is “what part of what you do would be hardest for others to copy, even if they knew exactly what you were doing?”

Our answers to that question are the topics explored in this letter. These areas fit into our operating philosophy: learn (research, research partners), build (Canvas, investing strategies), share (content), repeat.

What is common across these examples is slow, organic compounding. None of these assets could be air-dropped in, and they all feed off each other. These distinct areas of competitive advantage are working and have long runways, so it is unlikely that we launch a new large-scale effort in 2020. We’ve experimented enough over the years to know traction when we see it. We look forward to learning with you in 2020.

Happy New Year!

Patrick W. O’Shaughnessy, CFA

Chief Executive Officer and Portfolio Manager

Footnotes

1 Some important caveats to this “prediction.” Given the low effective sample size of the analysis--roughly 70 years, equivalent to only seven independent ten-year periods in the sample--it comes with a high degree of expected error. The fit is also in-sample, so the future correlation cannot be projected out with anywhere near the degree of tightness seen in the chart. Finally, we have to remember that forecasting methodologies based on valuation can only be accurately applied over very long horizons--longer than many of us are able to allocate based on. Today's valuation tells us very little about what's likely to happen to the market in the near-to-medium term.

2 In this chart, we show current period R&D, depreciation, and capex as a percentage of the sum of the absolute values of those quantities. We show the capex percentage as negative to contrast it with the R&D and depreciation. The black line shows the sum of R&D, depreciation and (negative) capex. When it's positive, the implication is that current expensing of investment is outweighing deferred expensing, increasing the chances that reported earnings are being understated. When the line is negative, the implication is that deferred expensing of investment is outweighing current expensing, increasing the chances that reported earnings are being overstated.

3 Also Because inflation, which upwardly distorts earnings from an accounting perspective, is lower than in the past.

General Legal Disclosures & Hypothetical and/or Backtested Results Disclaimer

The material contained herein is intended as a general market commentary. Opinions expressed herein are solely those of O’Shaughnessy Asset Management, LLC and may differ from those of your broker or investment firm.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by O’Shaughnessy Asset Management, LLC), or any non-investment related content, made reference to directly or indirectly in this piece will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this piece serves as the receipt of, or as a substitute for, personalized investment advice from O’Shaughnessy Asset Management, LLC. Any individual account performance information reflects the reinvestment of dividends (to the extent applicable), and is net of applicable transaction fees, O’Shaughnessy Asset Management, LLC’s investment management fee (if debited directly from the account), and any other related account expenses. Account information has been compiled solely by O’Shaughnessy Asset Management, LLC, has not been independently verified, and does not reflect the impact of taxes on non-qualified accounts. In preparing this report, O’Shaughnessy Asset Management, LLC has relied upon information provided by the account custodian. Please defer to formal tax documents received from the account custodian for cost basis and tax reporting purposes. Please remember to contact O’Shaughnessy Asset Management, LLC, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you want to impose, add, or modify any reasonable restrictions to our investment advisory services. Please Note: Unless you advise, in writing, to the contrary, we will assume that there are no restrictions on our services, other than to manage the account in accordance with your designated investment objective. Please Also Note: Please compare this statement with account statements received from the account custodian. The account custodian does not verify the accuracy of the advisory fee calculation. Please advise us if you have not been receiving monthly statements from the account custodian. Historical performance results for investment indices and/or categories have been provided for general comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your account holdings correspond directly to any comparative indices. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. O’Shaughnessy Asset Management, LLC is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. A copy of the O’Shaughnessy Asset Management, LLC’s current written disclosure statement discussing our advisory services and fees is available upon request.

Hypothetical performance results shown on the preceding pages are backtested and do not represent the performance of any account managed by OSAM, but were achieved by means of the retroactive application of each of the previously referenced models, certain aspects of which may have been designed with the benefit of hindsight.

The hypothetical backtested performance does not represent the results of actual trading using client assets nor decision-making during the period and does not and is not intended to indicate the past performance or future performance of any account or investment strategy managed by OSAM. If actual accounts had been managed throughout the period, ongoing research might have resulted in changes to the strategy which might have altered returns. The performance of any account or investment strategy managed by OSAM will differ from the hypothetical backtested performance results for each factor shown herein for a number of reasons, including without limitation the following:

▪ Although OSAM may consider from time to time one or more of the factors noted herein in managing any account, it may not consider all or any of such factors. OSAM may (and will) from time to time consider factors in addition to those noted herein in managing any account.

▪ OSAM may rebalance an account more frequently or less frequently than annually and at times other than presented herein.

▪ OSAM may from time to time manage an account by using non-quantitative, subjective investment management methodologies in conjunction with the application of factors.

▪ The hypothetical backtested performance results assume full investment, whereas an account managed by OSAM may have a positive cash position upon rebalance. Had the hypothetical backtested performance results included a positive cash position, the results would have been different and generally would have been lower.

▪ The hypothetical backtested performance results for each factor do not reflect any transaction costs of buying and selling securities, investment management fees (including without limitation management fees and performance fees), custody and other costs, or taxes – all of which would be incurred by an investor in any account managed by OSAM. If such costs and fees were reflected, the hypothetical backtested performance results would be lower. Therefore, it should be noted that on the previous pages of this presentation, any back-tested results may be reflected gross of fees. Had OSAM managed the back-tested Portfolio during the corresponding time period, the deduction of an OSAM fee would have decreased the reflected results. For example, the deduction of a 1.00% fee over a 10-year period would have reduced a 10% gross of fees gain to an 8.9% net of fees gain.

▪ The hypothetical performance does not reflect the reinvestment of dividends and distributions therefrom, interest, capital gains and withholding taxes.

▪ Accounts managed by OSAM are subject to additions and redemptions of assets under management, which may positively or negatively affect performance depending generally upon the timing of such events in relation to the market’s direction.

▪ Simulated returns may be dependent on the market and economic conditions that existed during the period. Future market or economic conditions can adversely affect the returns.

Composite Performance Summary

For full composite performance summaries. please follow this link: http://www.osam.com

O’Shaughnessy Asset Management – Canvas™ Disclosures

O’SHAUGHNESSY ASSET MANAGEMENT, L.L.C.

CANVAS™ INVESTMENT PORTFOLIO MANAGEMENT

CANVAS™ is an interactive web-based investment platform developed by O’Shaughnessy Asset Management, L.L.C. (“OSAM”) that permits an investment professional (generally a registered investment advisor) or a sophisticated investor to devise a desired investment strategy (“Strategy,” including any combination of such Strategies) for the professional’s client or such sophisticated investor. At all times, the investment professional, and not OSAM, is responsible maintaining the initial and ongoing relationship with the underlying client and rendering individualized investment advice to the client. In addition, the investment professional or self-managing sophisticated investor, as the case may be, and not OSAM, is responsible for (1) determining the initial and ongoing suitability of the Strategy for the client; (2) devising or determining the specific initial and ongoing desired Strategy; (3) monitoring performance of the Strategy; and (4) modifying and/or terminating the management of the client’s account using the Strategy. The client may not look to OSAM for, and OSAM shall not have any responsibility for: (1) providing individualized investment advice or making any determination as to the initial or ongoing suitability of any Strategy for any specific investor, including the professional’s client; (2) monitoring the Strategy; or (3) the performance of the Strategy. The use of the CANVAS™ platform does not serve as the receipt of, or as a substitute for, personalized investment advice from the client’s investment professional, for which the client must look solely to his or her investment professional. No guaranty of performance or suitability is made or may be inferred from materials at the CANVAS™ web site or the use of the CANVAS™ platform.

Past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. It should not be assumed that future performance of any specific investment or investment strategy, including the investments and/or Strategy devised and/or managed by OSAM, and any investment or investment Strategy resulting from the use of CANVAS™ , will be profitable, equal any historical performance level(s), be suitable for any specific investor or individual situation, or prove successful. Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of any or which would have the effect of decreasing historical performance results. When the securities to be purchased and held using the CANVAS™ platform include exchange-traded funds, including fixed-income funds, the investor will be subject to additional expenses imposed at the fund level; the CANVAS™ platform seeks to estimate these expenses but may not do so precisely. An investor’s account holdings will generally not correspond directly to any comparative indices or categories.

The CANVAS™ platform reports historical performance information for Strategies compiled by OSAM. These performance figures reflect hypothetical, back-tested results; thus, they represent the retroactive performance of simulated portfolios. As such, the corresponding results have inherent limitations, including that: (a) the results do not reflect actual trading using investor assets, but were achieved by means of the theoretical retroactive application of the devised Strategy, certain aspects of which may have been designed with the benefit of hindsight; (b) back-tested performance may not reflect the impact that any material market or economic factors might have had on the investment professional’s use of the hypothetical portfolio if the portfolio had been used during the period to manage actual investor assets; and (c) the back-tested performance of any Strategy does not reflect trading costs, investment management fees or taxes (although, as noted above, the expenses of exchange-traded funds included in any Strategy are sought to be taken into account). Such simulated theoretical returns are provided for informational purposes only to indicate historical performance had the Strategy’s portfolios been available over the relevant time period. OSAM did not offer the CANVAS™ platform until April 2019. Prior to 2007, OSAM did not manage client assets.

A copy of OSAM’s current written disclosure brochure is directly accessible via link at www.osam.com/brochure.

CANVAS™ is intended for use only by investment professionals and by certain other sophisticated investors with appropriate knowledge and experience who are able to bear the risks of loss associated with the use of the CANVAS™ platform.